Acknowledgement:

- In no way I would like to take any claim for the below finding. The below finding stuck me while re-reading all the interviews of Mr. Bharat Shah.

- The concept of Good Business and Bad Business is inspired from the post by Abhinav/Niren on Manufactured Luck blog here .

- The concept of Change in Intrinsic Value is inspired from Prof Sanjay Bakshi blog post “The Final Relaxo Lecture” in which he advices us to focus on expected return rather than on intrinsic value.

In my earlier post on “What causes Wealth Destruction over Long term? Lack of Growth and ROE below 15% or High Valuations?” I indicated that

For majority of the non-financial companies [with very few exceptions] common cause of wealth destruction is when Sales/PAT CAGR or ROCE or ROE average is lower than 15%. If all the four conditions are satisfied it’s highly unlikely [though there are few exceptions especially in metals & others] that wealth will be destroyed over a long period of time [5-8 yrs]. Am nowhere suggesting that if one has a Long Term view then one can buy at any price. What I am suggesting is IF ONE’S AIM IS NOT TO LOOSE MONEY, one should invest ONLY AND ONLY if one feels that company can sustain Sales/PAT/ROCE and ROE above 15% over long term basis

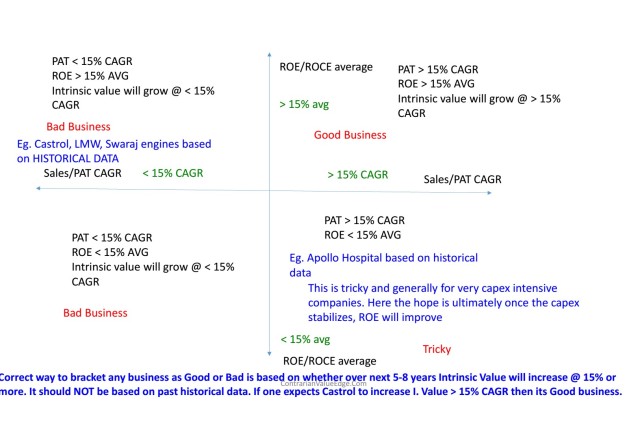

In the current post I am presenting more evidence that its the lack of sustainable growth over 15% over long term which causes destruction of wealth and NOT High Valuations. High Valuations will only result in low single returns for extended period of time. I have tried to classify all business on the basis of CHANGE IN INTRINSIC VALUE rather than abstract terms like High Quality, Low Quality, Cigar Butts, Deep value, High PE, Low PE, High Dividend yield etc.

You can download my study note from here or alternatively from here

Below are the finding based on my above study:

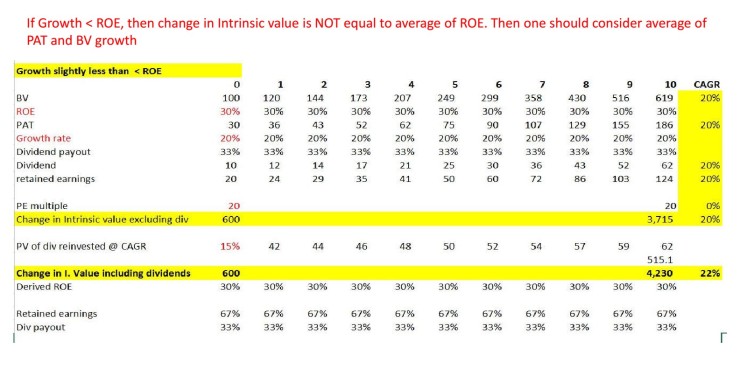

If Long term Growth < ROE, then change in Intrinsic value is NOT equal to ROE. In this case Change in Intrinsic Value is equal to average of PAT and Book Value CAGR

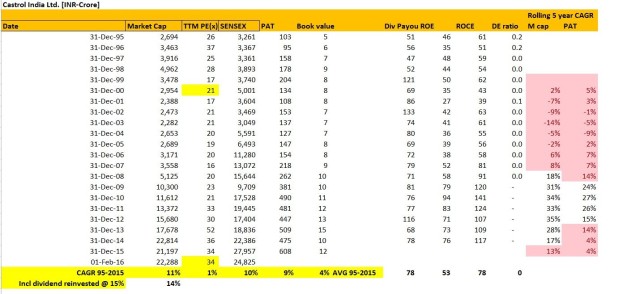

For companies like Hindustan Unilever and Castrol where PAT Growth is less than ROE, Growth in Intrinsic Value depends on PAT CAGR and not High ROE [even if its more than 50%]

To avoid Permanent Loss of Capital or Risk of Earning less than 15% Price CAGR, avoid investing in Bad Businesses. A Bad Business is any Business where Long Term Change in Intrinsic Value is less than 15% CAGR

I am classifying business as good or bad purely from investors perspective. For the society as a whole a business classified here as bad might be a good business and vice-versa

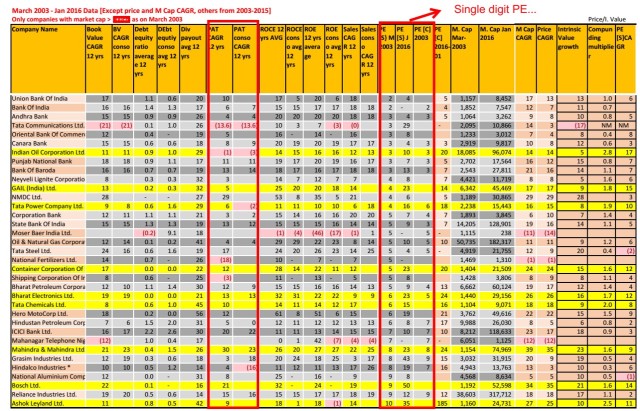

Unless Intrinsic Value grows at > 15% CAGR, Buying companies with Single Digit PE will NOT result in Price CAGR more than 15%

What causes PERMANENT LOSS OF CAPITAL? High Valuations or Lack of Sustainable Growth > 15% CAGR. Look for which companies are NOT PRESENT in this list and think Why?

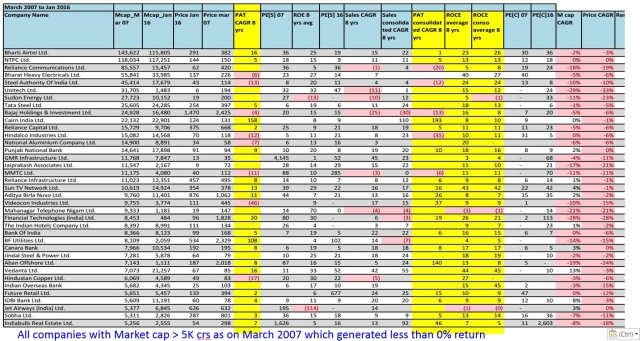

Companies which destroyed wealth between Dec 2007 and Jan 2016 [All companies with Market cap > 5K crs as on DEc 2007

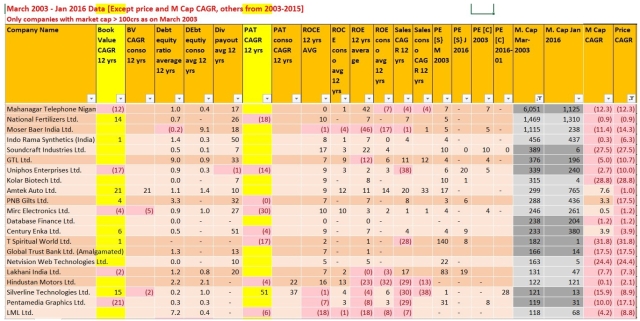

Companies which destroyed wealth between March 2003 and Jan 2016 [All companies with market cap of > 100crs as on March 2003

Hi Anil,

Really interesting analysis & conclusion.

1 question- If you have make error on one side- Growth or ROCE/ROE which one would be better based on past study?

or in other words, <15% growth or <15% ROCE/ROE, which one will hurt investors more?

LikeLike

Am travelling will post detailed response later…but knowingly I won’t commit mistake on either of the four important parameters… Else investment will ultimately prove to be failure for a buy and hold investors like me

LikeLike

Hi Anil,

Thanks for sharing really valuable and insightful analysis. however I am unable to understand your calculation of PV of dividend reinvested @ CAGR of 15%. Please guide.

LikeLike

I hv used compounding formula..anyhow that’s not important.. point is dividend won’t impact the ultimate returns much and there is always risk of ability to reinvest at higher rates….

LikeLike

Hi anil,

thanks for sharing this useful analysis.

keep up the good work.

LikeLike

Pingback: Lakshmi Machine Works – Process Vs Outcome | ContrarianValue Edge

Pingback: Turning Back Pages of My Investment Journal – Engineers India | ContrarianValue Edge

Hi Anil,

Extremely good work. I was wondering if you could have avoided the confusion of bad vs good ‘business’ by just calling it bad vs good ‘investment’. A great business (in terms of return on capital) might be poor investment because of either price or lower growth which leads to stagnant or lower intrinsic value growth.

Having said that, fascinating work. Cheers.!!!

LikeLike

Thanks Puneet….

My focus is to highlight that its safer to make money along with increase in intrinsic value of the business driven by profit growth and not merely on re-rating of business. Good businesses rarely result in permanent loss of capital…ofcourse to make money it also need to be a good investment. But first good business then price…

LikeLike